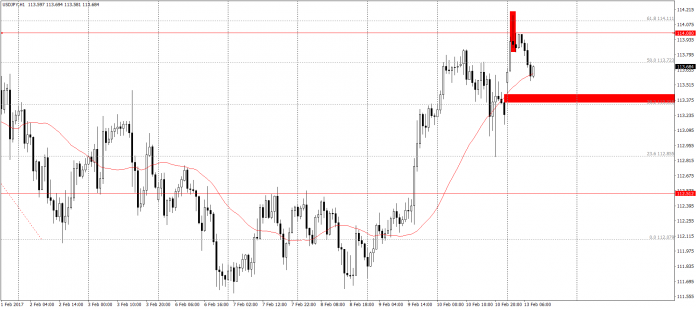

The most important Monday’s session macroeconomic publication came just before 1:00 our time. This refers to the forecasts of GDP for Land of the Rising Sun in the fourth quarter of last year. The results were worse than analysts’ expectations, which initially caused a stronger JPY weakness.

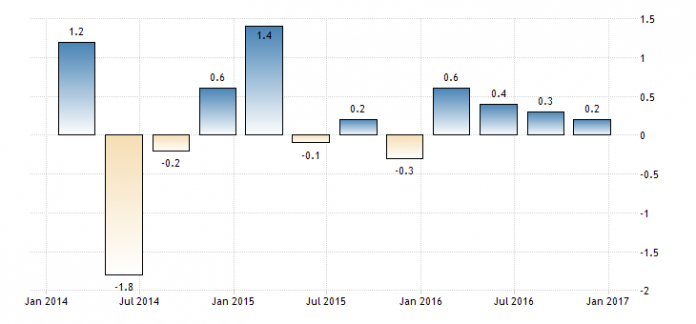

The dynamics of growth slows down to +0.2%

According to data from the Japanese statistical office, the latest forecast of GDP q/q Q4 shows dynamics of +0.2% to +0.3% from the previous quarter. In annual terms, while the growth rate was 1.0% (forecast 1.1%) – here a positive change, however it was upward correction of the result for the Q3 to 1.4%.

As can guess the outcome unfavorable to JPY contributed to the weakening of the local currency. The new week began with a small bullish gap, while the data caused appreciation of tens of pips. Further increases were blocked by a round level of 114.00, under which was set a bearish candle pin bar which stopped upward trend, but still the morning gap wasn’t closed.

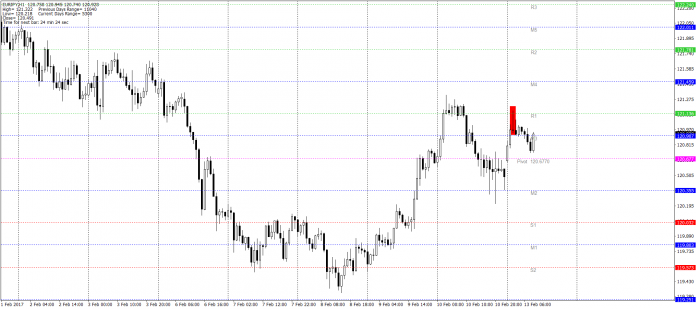

Situation on EUR/JPY looks very similar. Opening with a upward gap, two hours increases and bearish Pinocchio’s nose above the resistance – this time, however, the bulls were blocked by pivotal resistance R1:

In anticipation of the data from the Polish

Session February 13 does not offer too many macroeconomic data. About 08:00 we will know the results of German wholesale prices (change the dynamics on a monthly and annual basis), these are not so important for markets. In the afternoon, attention will return to Polish inflation and the current account balance – the Central Statistical Office reports on this issue should occur at 14:00.

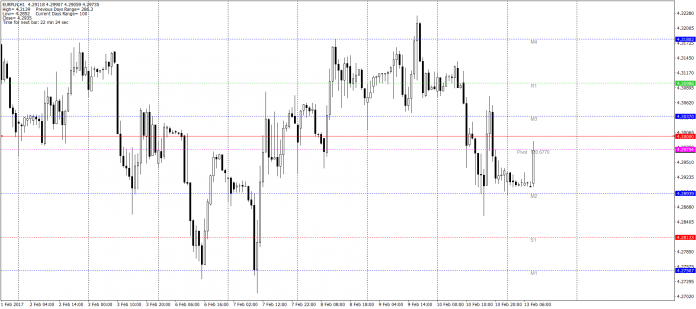

EURPLN in night did not show a stronger tendency to volatility by moving in a narrow channel, but the European morning brings a powerful movement against PLN. All the time we are, however, lower than 4.30, and additional resistance is the daily level of PP.

The most important data in the beginning week

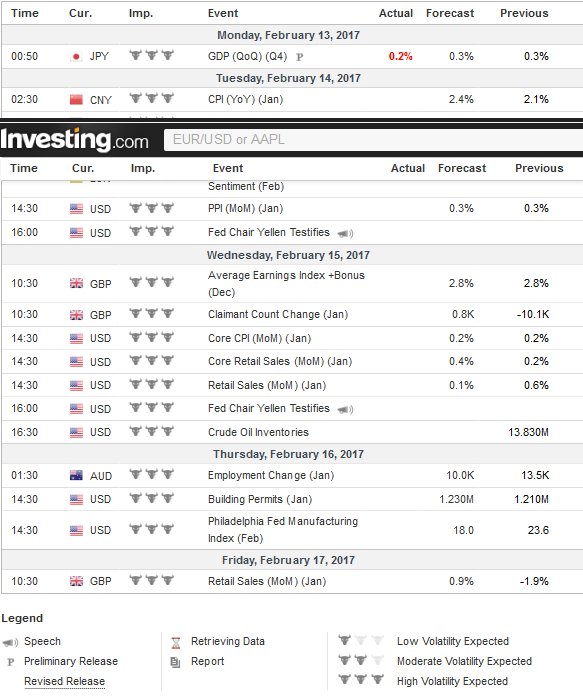

Below, a look at the calendar in the just beginning week. Tuesday’s session is primarily dominated by inflation data from Germany, UK and USA. February 15 (Wednesday) we will focus on the UK report from the labor market and a number of important US data – inflation, retail sales and stocks of black gold:

The last two days of the week will be definitely calmer – a report from the Australian labor market and the US Building Permits, and on Friday only UK retail sales.

Review")