During Asian sesison minutes of the last meeting of the Reserve Bank of Australia (RBA). Dovish comments on the economy and criticism of too strong Australian dollar led to depreciation of the local currency. Details inside macro morning commentary.

RBA: AUD too expensive because of rising prices on commodity market

After the absence of decision regarding changes in interest rates on Feb. 7, the RBA shared its protocols from the meeting. Here are some of the major headlines that could be found within the document:

- No changes on interest rates coincides with the current economic increases and inflation targets

- Further increase in AUD hinder the implementation of economic changes

- AUD grows supported by higher commodity prices on the commodity market

- Uncertainty as to the situation on the labor market

- Employment costs should increase gradually translating into competitiveness and retail inflation

- The downward inflationary pressures may be more difficult to defeat than expected

- A positive attitude about the Chinese GDP in 2017

In fact, no major news, full minutes can be read on the official website of the RBA. In a ANZ document with commentary published after the Bank of Australia is said that the AUD in the near future will be weaker – in connection with local fundaments and the further strengthening of the US dollar.

According to the latest projections of the bank price of AUD/USD is expected to fall to around 0.7200 at the end of this year – it should be noted, however, that compared to the previous projection the result is much better. ANZ previously suggested that in Q1 2018 Aussie will be worth 0.6800.

Looking at the chart of the Australian dollar, we see two waves of weakening. First right after the publication of minutes, the second at the beginning of the European session. Since the beginning of the day AUD/USD loses some dozens of pips:

Closing under short-term confluency of support levels certainly will open the way for further slippages. For AUD/NZD situation presents itself, however, quite the opposite. At the start of Tuesday’s session, we managed to overcome Friday’s peaks, which currently are tested from the top which could provide an opportunity to open long positions.

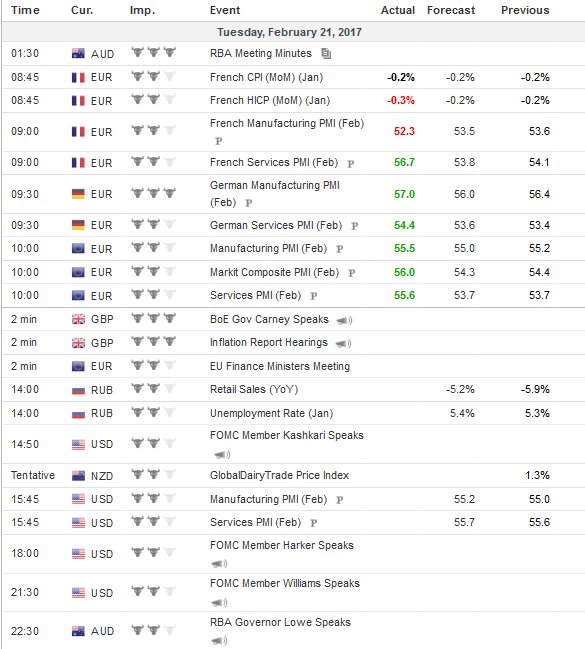

European PMI and other items on the calendar – session of February 21, 2017

At 10:00 will be announced preliminary results of the PMI industrial and service for individual European economies by Markit, which ultimately summarize publication covering the entire euro zone and the European Union. In addition, at 10:30 and 11:00 there will be publications directly from the UK. Mark Carney will speak on the BoE meeting on reports of inflation.

Further data only from 14:50 when on the podium arrives Kashkari from the Fed. About 15:45 the next dose of industrial and services PMI from Markit – this time for the United States.

Review")