![]()

![]() The spotlight today is on the release of the Sep ECB minutes (1330 CET). While historically these post-meeting minutes have had a pretty muted impact on EUR markets, this time could be different given (a) the heightened role of the currency and overall financial conditions in the ECB’s policy reaction function; and (b) the fact that discussions may hint at the Governing Council’s QE taper preferences.

The spotlight today is on the release of the Sep ECB minutes (1330 CET). While historically these post-meeting minutes have had a pretty muted impact on EUR markets, this time could be different given (a) the heightened role of the currency and overall financial conditions in the ECB’s policy reaction function; and (b) the fact that discussions may hint at the Governing Council’s QE taper preferences.

On the first point, we suspect the party line will be wariness over additional EUR strength. However, the recent focus on exogenous and endogenous drivers for the currency – and their differing macro implications – could see the discussions leaning towards acceptance of a strong EUR under certain economic conditions. This small shift in tone would be a giant leap forward for our bullish EUR view.

Get similar commentaries straight into your email inbox>>>

We doubt there’ll be too much in the way of exact details on how the ECB might taper its asset purchases. However, we now mainly see upside risks to the EUR from any policy announcement at the 26 Oct ECB meeting; the idea of a dovish – or more cautious – unwind of the asset purchase programme is embedded into markets. Signs that tapering could be more ‘punchy’ that what markets currently expect would lend support to a strong EUR heading into the Oct ECB meeting.

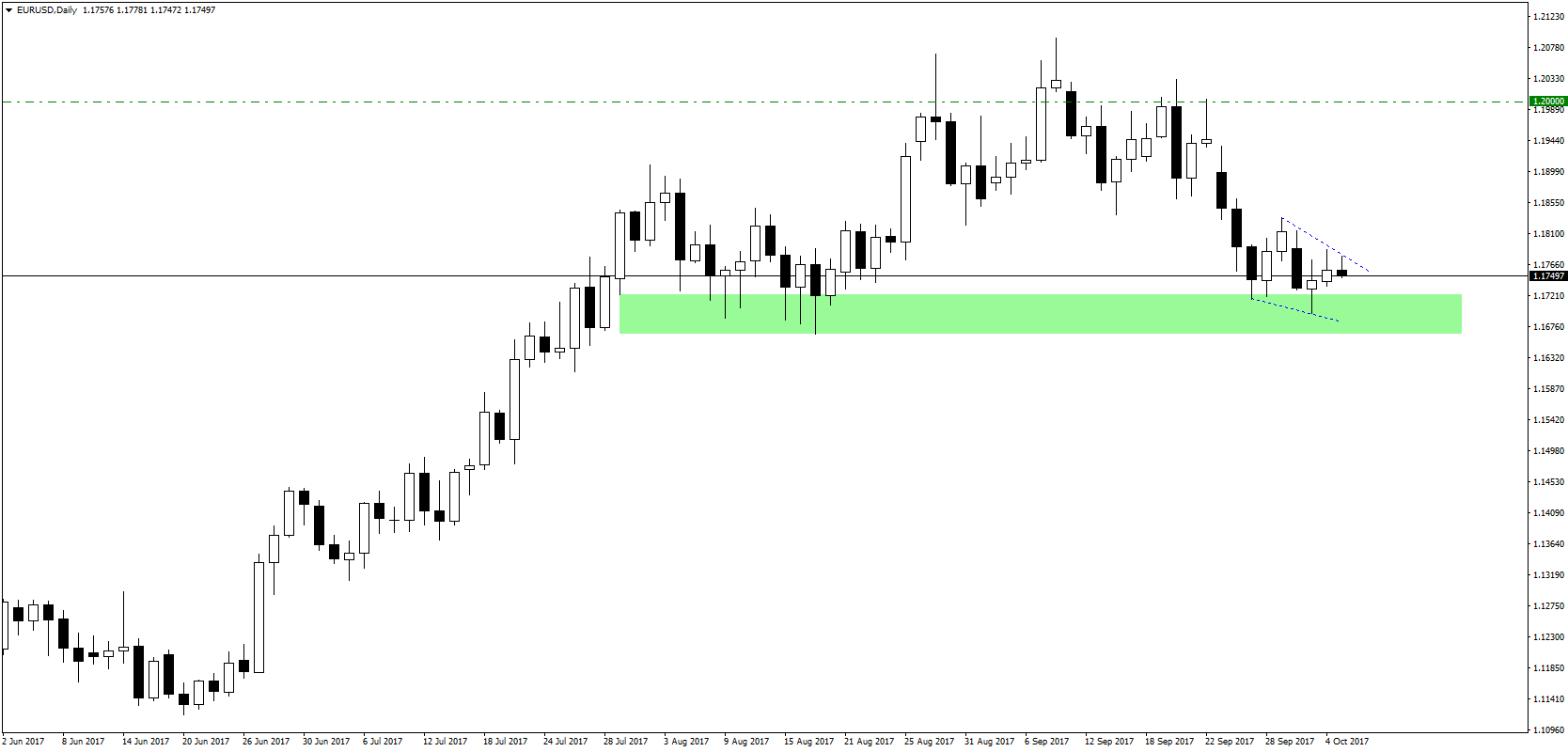

Political risks related to Catalonian independence remains the only catch to long EUR positions right now. Given the limited systemic risks to broader EZ financial markets, we think any fundamental EUR fallout is unlikely. Instead, were political noise to fade over the coming days or weeks, we would be inclined to enter long EUR positions against the USD, JPY and CHF. For EUR/$ we wouldn’t rule out a move above 1.20 on the prospects of a more aggressive ECB QE taper plan.

Political risks related to Catalonian independence remains the only catch to long EUR positions right now. Given the limited systemic risks to broader EZ financial markets, we think any fundamental EUR fallout is unlikely. Instead, were political noise to fade over the coming days or weeks, we would be inclined to enter long EUR positions against the USD, JPY and CHF. For EUR/$ we wouldn’t rule out a move above 1.20 on the prospects of a more aggressive ECB QE taper plan.

Review")