The first week of May promises to be very interesting. Although Monday will not bring us much excitement due to the Labour Day celebrations in most countries in Europe and Asia, already on Tuesday the Reserve Bank of Australia (RBA) will announce its interest rate decision at 6.30am.

Tuesday 2 May

The market expects the RBA to maintain current interest rates at its meeting this week, similar to the decision made at its last meeting. Despite persistently high inflation in Australia, there are indications that it may have peaked, prompting the Bank to adopt a wait-and-see approach in assessing the effects of monetary policy decisions. In line with Governor Lowe’s comments following the last RBA meeting, keeping rates unchanged does not necessarily mean that the hikes are over.

Later in the day, we will learn PMIs from Germany (9:55) and the UK (10:30). At 11:00 – inflation data from the European Union. A slight increase to 7.0% is expected, compared to the previous 6.9%. Particularly the latter data may influence increased volatility on the EUR in view of Thursday’s ( 4 May) ECB meeting and the decision on the euro area’s main refinancing rate.

In the afternoon at 16:00, the JOLTS report from the US. For the March JOLTS Job openings data, the consensus is for a drop to 9.74M from 9.93M, but Citi analysts expect a slight increase to 10.1M after a surprise drop in February. Even with this decline, job openings are now above pre-pandemic levels.

The survey was conducted by the US Bureau of Labor Statistics to measure job openings. It collects data from employers on their hiring, vacancies, recruitment, hires and separations.

JOLTS defines Job Openings as all positions that are open (unfilled) on the last business day of the month. A job is ‘open’ only if it meets all three of the following conditions:

A specific position exists and there is work available for that position.

The job could start within 30 days, regardless of whether the workplace finds a suitable candidate within that time.

There is active recruitment of workers from outside the location of the establishment where the position is located.

A reading stronger than forecast is generally supportive (bullish) for the USD, while a reading weaker than forecast is generally negative (bearish) for the USD.

Wednesday 3 May

Wednesday 3 May

On Wednesday, New Zealand will publish q/q employment change and the unemployment rate. In the US, the ADP Non-Farm employment change and ISM Services PMI will be published, followed by the FOMC statement, the federal funds rate and the FOMC press conference. Of these events, ADP and the FOMC are particularly noteworthy.

The ADP data usually has an impact on gold, EUR and JPY, but the impact is usually short-lived and the market can return to pre-data levels after a few hours.

Of course, the event of the day will be the Fed’s evening (20:00) decision on interest rates in the US. The market expects a 25bp rate hike at the next FOMC meeting, followed by a pause to assess the effectiveness of current monetary policy. Chair Powell is likely to be asked about a possible end to the hike cycle, but he is likely to reiterate that the Fed’s approach is data-dependent and avoid a straightforward answer. The meeting may also include questions about ongoing stress in the financial (banking) sector.

Thursday 4 May

Thursday will bring the Eurozone’s main refinancing rate, the monetary policy statement (14:15) and the ECB press conference at 16:00. Eurozone inflation data (Tuesday at 11:00) will be in focus, as it may provide insight into the upcoming ECB meeting on Thursday. Following a rise in core inflation in March, ECB chief economist Philip Lane stressed that further tightening is likely, stating that “current data indicate that we should raise rates again”. The market consensus is for a 25bp rate hike at the May meeting, followed by another 25bp hike in June. Headline y/y inflation data for April is expected to be higher than in March.

Friday 5 May

Friday 5 May

Payrolls day, the US labour market report – as usual, we expect high volatility on financial instruments. Despite the mixed recent data, the US labour market remains strong. Analysts predict that new hire growth will slow from 236K to 180K, while average hourly earnings m/m are expected to remain stable at 0.3% and the unemployment rate is expected to rise from 3.5% to 3.6%.

“The labour force participation rate also increased for the fourth consecutive month,” – Wells Fargo analysts said. “However, falling hiring intentions and job openings indicate that demand for workers will continue to decline.”

At the same time, data from the Canadian labour market will also be known. For the Canadian economy, employment change is expected to fall from 34.7K to 22.6K and the unemployment rate to rise from 5% to 5.1%.

The week, despite being a little shorter due to Monday’s holiday, promises to be very interesting and could bring quite a bit of change to the charts.

LIVE EDUCATION SESSIONS

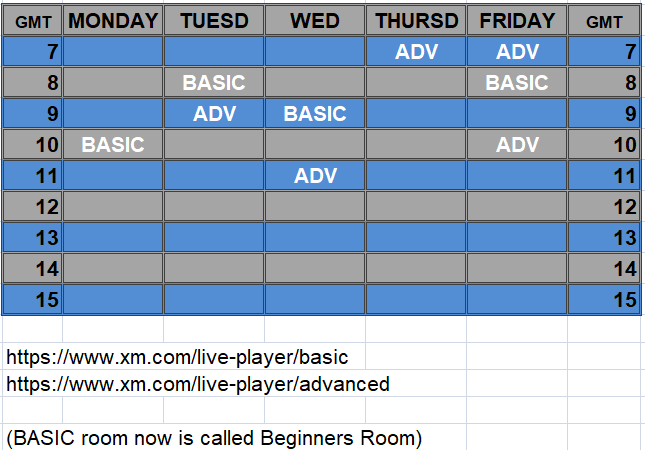

This WEEK (1-5 May) I am pleased to invite you to several online sessions. Below is the schedule of meetings:

Links: BASIC (beginners room) ADVANCED ROOM

The above analysis is based on the PA+MACD strategy, a detailed description of which you can read HERE . I will talk more about the PA+MACD strategy applied to these currency pairs during the live trading sessions which you can attend from Monday to Friday.

More current analysis on the group : Trade with Dargo

In our Facebook group, which you can join anytime: https://www.facebook.com/groups/328412937935363/ you will find 5 simple strategies on which my trading is based. There, every day we post fresh analyses of currency pairs and commodities. You can also visit my channel where I post my trading ideas: https://t.me/TradewithDargo

In our Facebook group, which you can join anytime: https://www.facebook.com/groups/328412937935363/ you will find 5 simple strategies on which my trading is based. There, every day we post fresh analyses of currency pairs and commodities. You can also visit my channel where I post my trading ideas: https://t.me/TradewithDargo

Review")