We have entered the second half of 2023. Here is a brief overview of what the central banks of the world’s major economies may be planning in the coming months:

US Federal Reserve

In June, rates remained unchanged at 5.25%. However, markets expect a rate hike in July. There is still plenty of time until the July 26 decision. Before that, there will be a lot of important data coming, in particular the labour market data – payrolls on Friday this week and US CPI data, which will be released on July 12. Recent readings indicate a steady decline in inflation, which currently stands at 4%. Futures contracts ( July 3 data) on the Fed interest rate show the odds of a 25 basis point rate hike at ~90%. The remaining ~10% is betting on a decision of no change.

European Central Bank

Policymakers raised rates by 25 bps to 4% on June 15 and almost preemptively pledged to raise rates by another 25 basis points at their July 27 meeting.

The markets took full note of the decision. The question remains whether they will continue tightening policy in September. The latest inflation data continues to show that core inflation remains stable. This leads the market to expect another 25-basis-point rate hike after the summer.However, at the end of Q2, the economy is starting to roll over again. The manufacturing sector is already in recession, and services are starting to stutter.

If the trend continues, the ECB will have to find a golden mean on this issue.

Bank of Japan

There has been no change in the bank’s policy since new Governor Ueda took office. This has caused yen bulls to become increasingly frustrated

As a result, we have seen a dramatic decline in the yen against the euro and pound in particular. USD/JPY has also reached the territory of possible intervention near 145.

So far, there have been no major signals that could augur a change to a more restrictive policy in the short term. Interest rates in Japan are -0.1% and have not been changed since 2016.

However, there are some areas of the market that are expecting a potential change in the YCC in July.

If that doesn’t happen, expect the yen to fall further as market frustration builds and the BoJ possibly attempts to rescue the exchange rate through interventionist yen purchases.

Bank of England

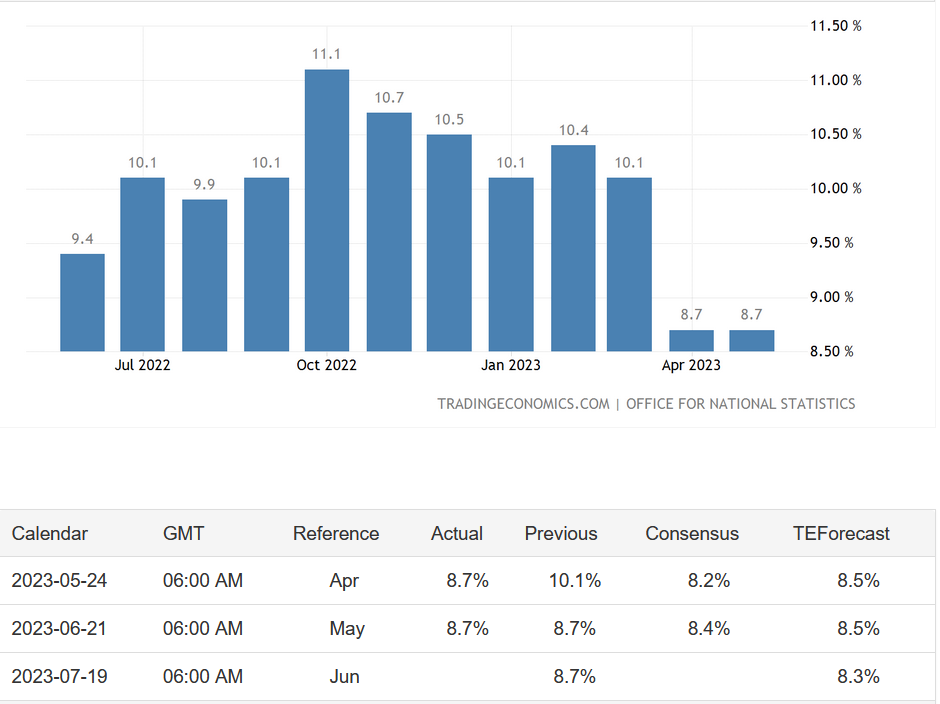

Inflation continues to be a problem, as it remains high at 8.7%.

The cost of living crisis continues, affecting economic conditions

This results in a growing risk of stagflation, which is a macroeconomic phenomenon involving the simultaneous occurrence of both significant inflation and economic stagnation in a country’s economy. The causes of this phenomenon are attributed to a negative supply shock, which causes both an increase in prices and a reduction in production. The BOE must try to conduct a soft landing. So far, policymakers have made it clear that their main goal is to counter inflation. But if this risks destroying the economy, further rate hikes could be bad for sterling.

A 25 basis point rate hike in August is now fully priced in, with markets even leaning toward a 50 basis point move. The chances of the latter are currently ~83%.

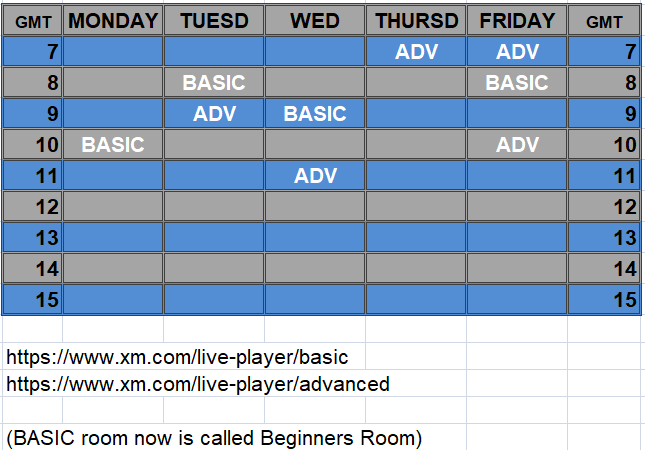

LIVE EDUCATION SESSIONS

This WEEK (3-7 July 2023 ) I am pleased to invite you to several online sessions. Below is the schedule of meetings:

Links: BASIC (beginners room) ADVANCED ROOM

The above analysis is based on the PA+MACD strategy, a detailed description of which you can read HERE . I will talk more about the PA+MACD strategy applied to these currency pairs during the live trading sessions which you can attend from Monday to Friday.

More current analysis on the group : Trade with Dargo

Review")