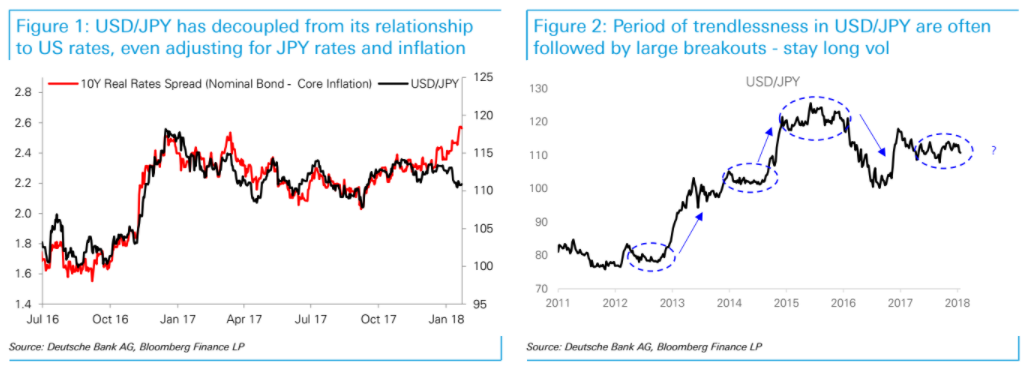

The JPY has not been behaving itself this year, decoupling from its famous relationship with US yields. US 10Y nominal yields and the US-Japan 10Y real rate spread would both be consistent with USD/JPY at 117-118, based on “old” correlations (Chart 1). Something has changed. The popular contention is the market is starting to price some BoJ normalization after a small reduction in long- end JGB purchases, TIBOR rates edging higher, and subtle language changes in Kuroda speeches. We make three points in response, ahead of the BoJ meeting tomorrow…

The JPY has not been behaving itself this year, decoupling from its famous relationship with US yields. US 10Y nominal yields and the US-Japan 10Y real rate spread would both be consistent with USD/JPY at 117-118, based on “old” correlations (Chart 1). Something has changed. The popular contention is the market is starting to price some BoJ normalization after a small reduction in long- end JGB purchases, TIBOR rates edging higher, and subtle language changes in Kuroda speeches. We make three points in response, ahead of the BoJ meeting tomorrow…

This JPY strength is not alarming

The JPY TWI is not actually stronger, as JPY is simply participating in, rather than leading USD weakness now. Second, the Japanese equity market is sustaining gains, a phenomenon which began last year as the baton passed from QE-driven to earnings-driven gains. Equities are not scared of a stronger JPY, if the reasons for JPY strength are a stronger economy. Finally, even with a faster stealth taper this year, the BoJ’s balance sheet will likely expand by 6% of GDP, relative to a contraction of 3% of GDP at the Fed. The relative punchbowl is still enormous.

Watch inflation insights from BoJ

The real lynchpin to a BoJ tightening narrative will come from inflation, given the singular focus on the price stability mandate. In BoJ’s last Outlook Report, CPI was seen as showing “relatively weak developments” and 6 out of 9 board members saw downside risks to their long-term forecasts. BoJ also felt “inflation expectations remained in a weakening phase.” While they are unlikely to upgrade inflation forecasts tomorrow, their language will be watched. Japan 10Y breakevens are testing the top of their 2Y range, and oil prices are included in core inflation in Japan. The next inflation numbers are due on Friday, with the market watching whether core can move above 1% (last 0.9%). Our economists believe it needs to print above 1% for 3-6 months for BoJ to consider a policy adjustment.

Stick with the higher vol trade

As we argued in our FX Blueprint, long periods of trendlessness in the JPY have often been followed by breakouts. After trading in a dull 110-115 band for 80% of 2017, it is natural for USD/JPY to start to test its range-bound regime (Chart 2). This should mean that the hurdle for a catalyst is quite low, with markets willing to chase small shifts. We like the higher vol trade in Japan, and continue to hold onto our mid-dated strangles and FVAs recommended in the Blueprint.

Review")