![]()

![]()

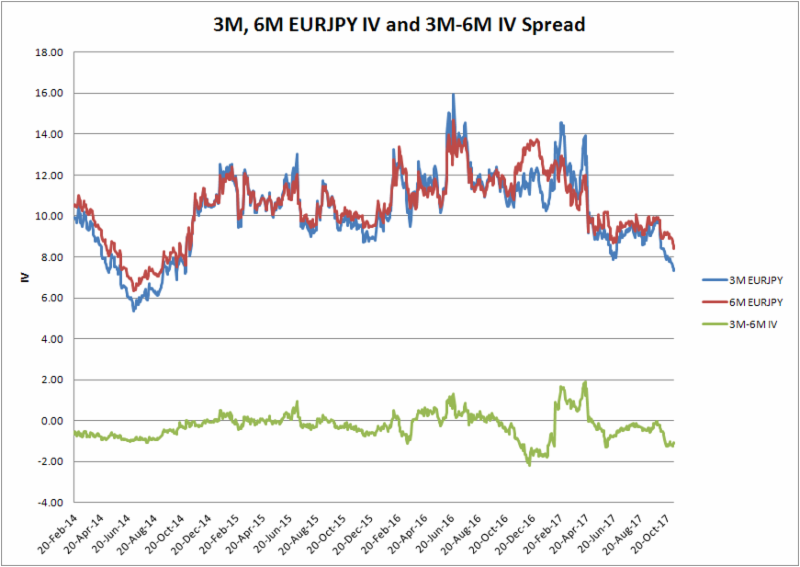

The chart above is EURJPY implied vol going back to 2014. Three-month EURJPY is in blue and six month is in red and the spread (3M-6M) is in green below. The spread between 3M and 6m EURJPY implied vols has widened out to over 1 vol and this presents a number of useful calendars spread opportunities to views that both on the direction and the shape of the vol curve. The most obvious spread is to buy the 3M and sell the 6M in a ratio that keeps the spread vega neutral, or to take the view that the spread will steepen on a renewed EURJPY weakness, a more directional trade would be to buy 3M 130 Yen calls X2, and sell X1 6M 128Yen calls. The pricing on this would be to pay approx 1.29% of EUR for the 3M and earn the same in the six months. If done in a ratio (2X by 1X) this would be a net debt of approx 1.29% of EUR.

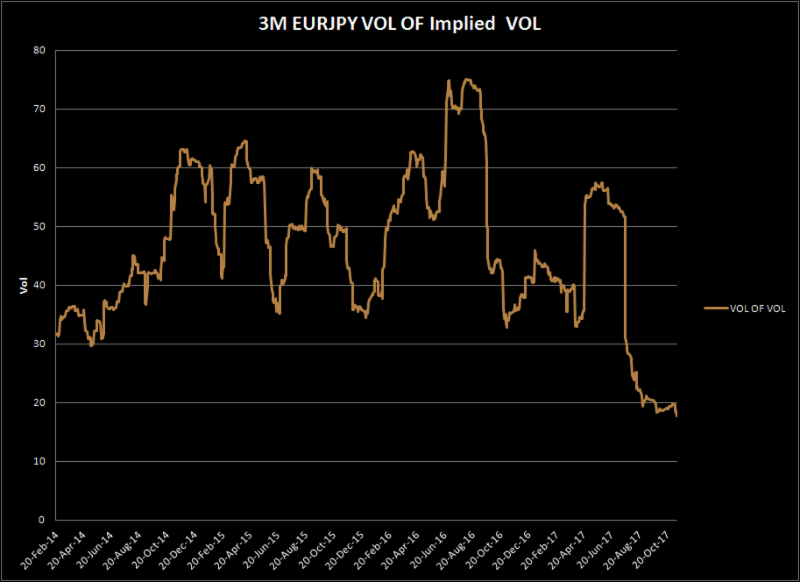

The volatility of volatility is also a useful indicator to look at particularly when it reaches an extreme. This is the case now with EURJPY three month implied vol and at a minimum suggests higher EURJPY volatility ahead.

Last week we suggested buying 3M EURJPY strangles and this week we are (above) suggesting EURJPY calendar spreads either in a vega neutral 3M vs 6M spread or as a diagonal, buying 3M 30Delta Yen calls and selling half the amount of 6M 30 Delta calls.

Last week we suggested buying 3M EURJPY strangles and this week we are (above) suggesting EURJPY calendar spreads either in a vega neutral 3M vs 6M spread or as a diagonal, buying 3M 30Delta Yen calls and selling half the amount of 6M 30 Delta calls.

GBPJPY dispersion is now close to a cyclical low which suggests the consolidation pattern that we have seen in the past six weeks is now close to an end. The spot is holding the hourly trend line support in the chart above, and a break should trigger a much lower move to support the 140 level. This pattern is also evident in CADJPY as well and suggests a more generalized rise in the Yen on the major crosses.

One month and three-month GBPYEN risk reversals moved lower on the week as better bids came in for Yen calls. This pattern was also seen in USDJPY & CADJPY.

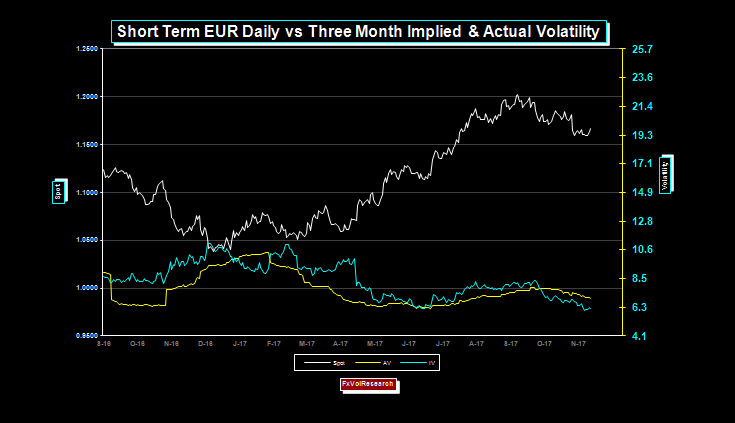

The gradual and sustained rise in EUR volatility that we have seen since mid-June/July of this year has given way to a declining trend and we are nearly back to the lows of the year. Notice at the same time that IV-AV spreads are now negative, and this indicator combined with the low percentile ranking of the implied is another metric we use to assess the cheapness of the premium levels in the options market.

EUR momentum remains in negative territory while the spot is confined to a clear down channel. The market is placing too much emphasis on the tax bill in front of the US Congress. It is likely to go nowhere fast. Interest rate differentials are more likely to fuel a more sustained correction in the EUR lower and this correction should justify a more sustained move higher in the medium term. This kind of price action will also lead to a pick up in EUR vols.

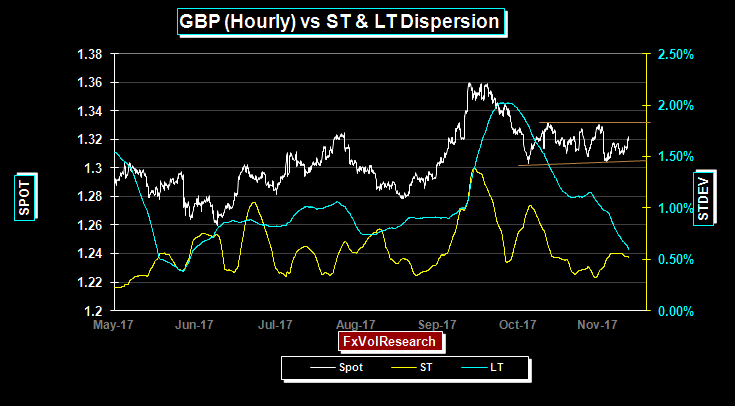

GBP remains in a sideways consolidation pattern that is consistent with the decline in the dispersion readings. The spot has found good support at 1.3050 and resistance at 1.3300. Dispersion could easily continue to decline near term, but over the balance of the year, GBP is likely to break this channel pattern. Two week and one month GBP options are not underpriced in relations to realized vols.

Get more reports on FxVolResearch.com!

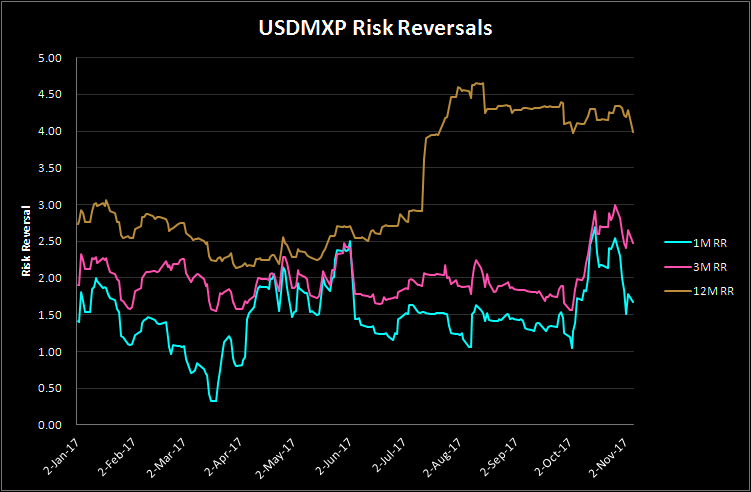

MXP risk reversals moved lower on the week with US call losing some of their premium vs US Puts.

MXP continues to fail to take out the 19.25 level and now is showing clear signs of momentum divergence.

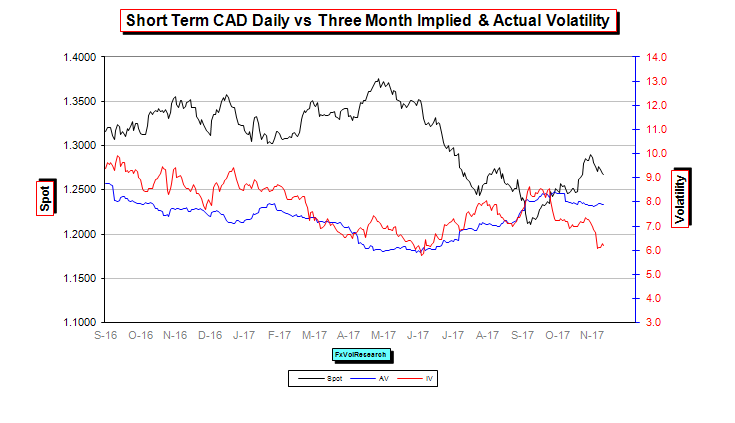

If you have been following this commentary, we have been recommending strategies that are short CAD implied vol and at the same time bleed shorter CAD as a result of decay. The CAD vol curve has moved sharply lower, and in the 3M part of the curve is close to testing levels around 6% where it has usually found good support. We would be inclined to cover short vol positions under the 6% level in the coming weeks.

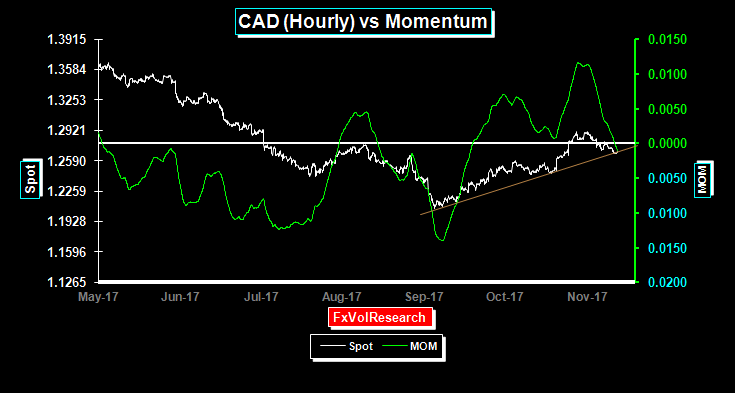

CAD is still holding on to the hourly trend line in the chart above and momentum has moved into neutral territory. The commodity price indexes are still providing underlying support however short-term yield spreads continue to favour the US$. The market has not yet entirely dismissed the notion that the BoC can engineer another rate hike by the end of the year. This fears should be put to bed once we see the next batch of inflation reports in the coming week. Once this fear is dispelled we would expect a move back to 1.3000 and an unwinding of the long CAD positioning in the leveraged community.

Previous Weekly FX Review

Best Regards,

James Rider

Director,

FxVolResearch Ltd.

Review")