![]()

![]()

Equity investors entered the third quarter with an optimistic attitude. Despite the low trading volumes and shortened U.S. trading session, stocks across Europe and the U.S. posted considerable gains sending the Dow Jones industrial average to a new record high with the financial and energy sectors taking the lead. Data released on Monday supported the appetite to risk as factories in the Eurozone and the U.S. surprised to the upside. The U.S. manufacturing index rose to 57.8 from 54.9 in May, the strongest expansion since August 2014. Similarly, IHS Markit’s Manufacturing PMI for the eurozone rose to 57.4, the highest since April 2011.

The positive data sent the yields on U.S. 10-year Treasury bonds to highest levels since mid-May, and on the shorter end, 2-year Treasury Notes mainly influenced by monetary policy actions rose to highest levels since the global financial crisis. This move convinced the dollar bulls to return after investors dumped the U.S. currency for four straight months. Whether the spike in the U.S. dollar is meant to resume or just a dead cat bounce depends on how fast other central banks across advanced economies converge into normalization, but on the shorter run, Wednesday’s FOMC’s minutes and Friday’s jobs report will be the prime catalyst. Currency markets are trading in a very narrow range early Tuesday, and I expect traders to remain on the sidelines until the U.S. return from the Independence holiday on Wednesday.

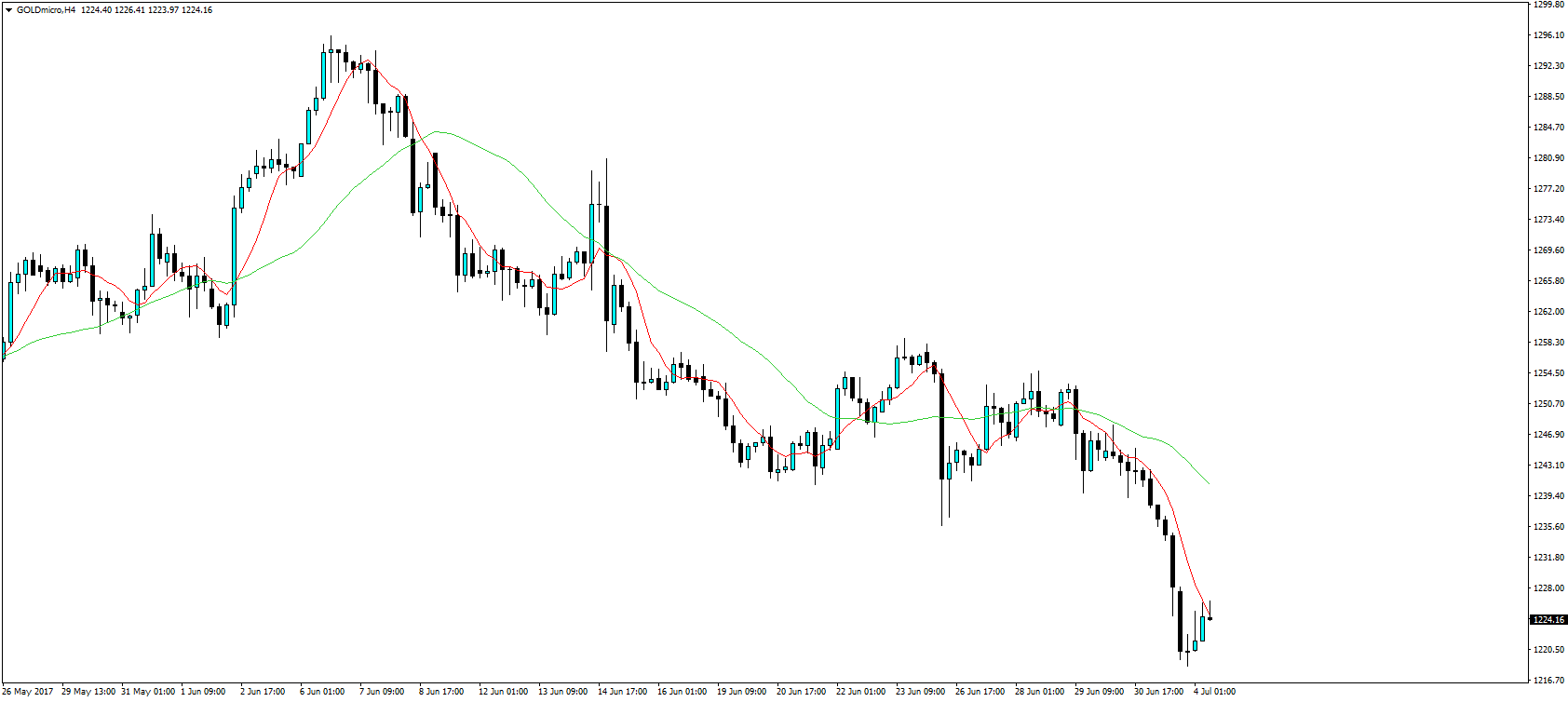

Gold was the biggest story yesterday. The yellow metal has lost its shine posting its biggest one-day fall in almost 8-months. The dollar’s strength may have contributed to the selling pressures, but I think it was only a minor factor. Many investors believe that the bull bond market has come to an end as central bankers signaled borrowing costs are going up, which going forward will be the major factor impacting precious metals. Breaking below the 200-days moving average also attracted bears to drag prices lower, with the immediate support now seen at $1,213.80 (May’s low). However, if Beijing-Washington tensions escalated after a $1.4 billion U.S. arms sales to Taiwan and sending a navy missile destroyer close Triton Island in the South China Sea, investors will always return to gold for protection from political risks. Today’s launch of a ballistic missile from North Korea also added to the complications of China-U.S. relations, but it seems markets did not take it as a serious threat. Overall, macroeconomic fundamentals are indicating lower gold price, while geopolitical risks are keeping the Bulls on standby.

Review")